Selling KL to reduce the office space overhang

Cover Story: Selling KL to reduce the office space overhang

Kamarul Azhar/The Edge Malaysia

September 01, 2022 14:00 pm +08

This article first appeared in The Edge Malaysia Weekly, on August 22, 2022 – August 28, 2022.

EARLY this month, a group of journalists were invited to the PNB Merdeka 118 tower that, upon completion, will be the second tallest building in the world. At 118 floors, it will tower over all else in Kuala Lumpur, including the newly completed Exchange 106 in Tun Razak Exchange (TRX) with its gleaming crown.

The view from the 116th floor of Merdeka 118 where the observation deck will be located is, as expected, fantastic. Almost the entire city and beyond can be seen, although from that height, everything looks small and insignificant — with the exception of the 106-storey Exchange 106 and the 26-year-old Petronas Twin Towers.

The Merdeka 118 tower has approximately 1.7 million square feet of net lettable area (NLA) and the occupancy rate is picking up steadily, according to PNB Merdeka Ventures Sdn Bhd, the real estate arm of Permodalan Nasional Bhd (PNB) that owns the development.

“Upon completion, we expect the occupancy to be at about 70%. We are currently in advanced discussions with a number of major domestic and international corporations to be tenants in the Merdeka 118 tower,” the company says.

PNB will have few difficulties filling up the space at Merdeka 118 as some of its investee companies, including Malayan Banking Bhd, are expected to be moving into the tower.

The Exchange 106 tower, which is the centrepiece of the 70-acre TRX development, once completed, would offer 2.6 million sq ft of NLA. This would add to the supply of office space in KL, although Exchange 106’s unbeatable address could make it more desired than other office buildings in the city.

But the fact is, this will create vacancies elsewhere as Merdeka 118 and TRX’s office buildings are coming into an already saturated office space market in KL.

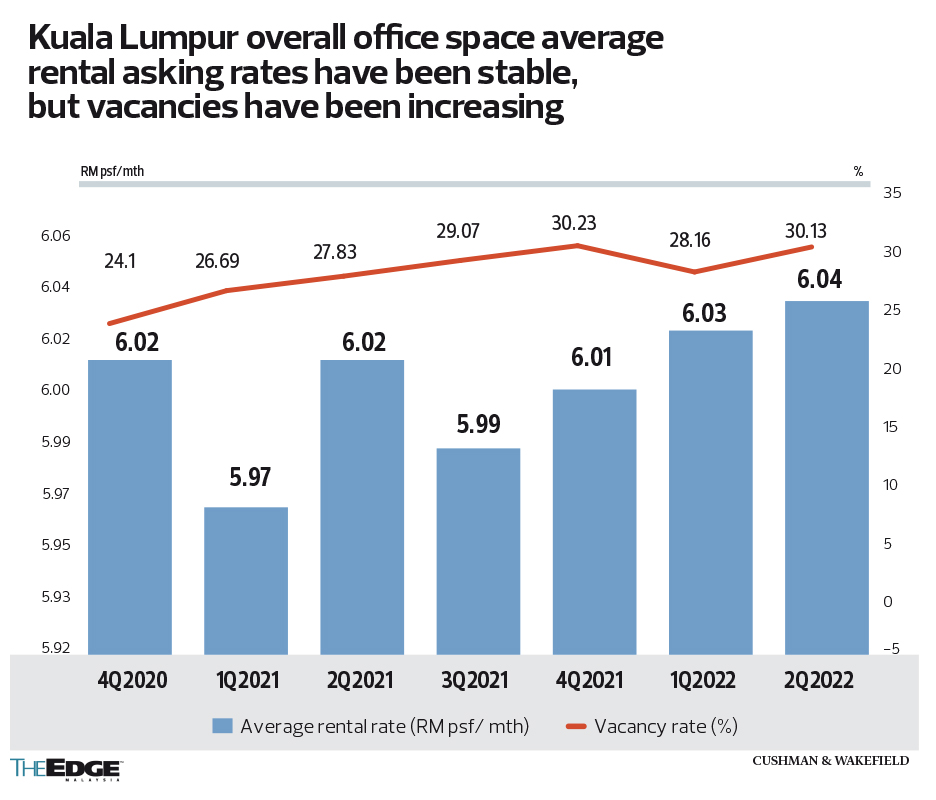

According to data from the National Property Information Centre (Napic), the vacancy rate of purpose-built offices (PBO) in KL has been above 20% since 2016.

Napic data shows that the vacancy rate of PBOs in KL stood at 26.67% in 2021, the highest level since 2001 when the vacancy rate stood at 27.4%. It inched up even higher in the second quarter of 2022, with Cushman & Wakefield estimating the vacancy rate at 28.3%, higher than in 2001.

Note that the latest data does not include the mammoth Merdeka 118 and TRX as the offices at these two major developments have yet to be completed. Merdeka 118 is expected to be completed by the end of this year, while several office buildings in TRX, such as the Affin Bank Tower, are also set to be completed this year.

Oversupply to persist, but Prime and Grade A offices in short supply

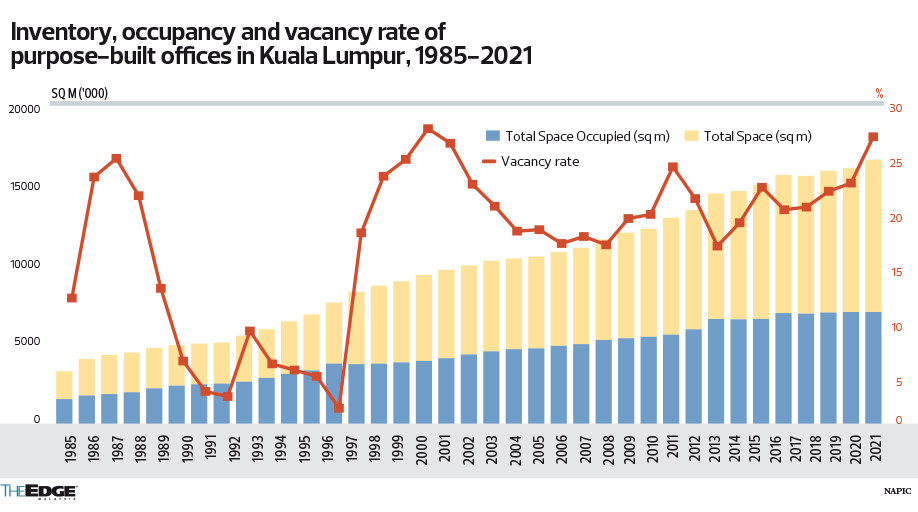

According to Cushman & Wakefield, planned and under construction office spaces in KL’s central business district (CBD) as at 2Q2022 stood at 9.37 million sq ft. Including those in the fringe areas of KL Sentral, Pantai, Bangsar and Damansara Heights, the figure goes up to 11.27 million sq ft.

Based on the inventory level of 106.13 million sq ft of office space in KL (CBD and fringe), the planned and under-construction supply make up 10.62% of the current inventory.

With the vacancy rate on an upward trend since 2017, it is clear there is an overhang of office space market in KL. While office space developments have been slowing due to the oversupply situation, the current high vacancy rates must be addressed.

“The oversupply of office space has been plaguing the market for years and, looking at the list of projects, this may persist,” says Foo Gee Jen, chairman of CBRE | WTW, in an email to The Edge last Thursday.

“The situation will worsen as ageing buildings are unable to provide the latest office requirements like availability of high-speed internet, environment-friendly features, poor ventilation and lighting. For example, along Raja Chulan, there are buildings completed in the 1990s and 1980s with an occupancy rate of less than 50%,” says Foo.

He adds that the latest office requirements have initiated tenants’ movement from old buildings to newly developed properties, creating a new demand for office space in the market. The rising awareness of environment, sustainability and governance (ESG) has created the demand for this kind of office space, which is limited in supply.

“Take-up for buildings built with the latest infrastructure and green elements is good, where most of the buildings recorded higher occupancy rates; some are fully occupied. Newer buildings like IQ Tower and Affin HQ at TRX, 1Powerhouse at Bandar Utama and iMazium at Uptown are in good demand and achieved good take-ups,” says Foo.

This movement from old buildings to new ones offering amenities suitable for a modern, sustainability-minded and technology-driven business has led to high take-up rates for newer office buildings, but left older ones vacant.

And if nothing is being done to refurbish or redevelop these older buildings, owners of these assets may find themselves in a quandary.

Meanwhile, strategic land banks within KL are becoming scarcer by the day. Therefore, developments of newer offices that incorporate ESG aspects lag demand, which in turn could make KL less attractive than its peers such as Singapore and Bangkok. In Southeast Asia, Singapore is the undisputed regional hub for many multinational corporations (MNCs), even though the city-state is one of the world’s most expensive locations.

In the 2022 Cost of Living City Ranking by Mercer, Singapore is ranked eighth in the world for international employees’ cost of living, being more expensive than Tokyo, Shanghai, London and Los Angeles.

Meanwhile, KL is ranked 181, below even Bandar Seri Begawan, Brunei, at 179. All other major cities in Southeast Asia are deemed more expensive than KL — above it is Ho Chi Minh City (163), Vientiane (157), Jakarta (151), Hanoi (150), Phnom Penh (134), Manila (122) and Bangkok (106).

With the city having world-class infrastructure, a melting pot of cultures with an international outlook, availability of good talents, and strong government support for business and industries, some may find it hard to comprehend why KL still lags behind Singapore when it comes to MNCs setting up regional hub operations.

It is not too farfetched to say that Malaysians have an overoptimistic perception that KL will be the natural location for MNCs to set up their regional hubs in this region due to the strengths that it has — good infrastructure, multilingual workforce, relatively good quality of life, and low cost of living and so on. And this, perhaps, has inadvertently translated into the oversupply of office space in the city, as real estate developers and policy makers envisioned KL offices as being highly sought after. This can be seen in the TRX development, which was designed specifically to be a financial hub for the region.

However, until today, financial institutions that have taken up plots in TRX are Affin Bank, Prudential, Lembaga Tabung Haji and HSBC — all are building their new headquarters there, leaving behind their old headquarters elsewhere in the city.

It is not known whether other financial institutions will be making TRX their home.

With all this in mind, Malaysia needs to do more to attract MNCs to set up their regional hubs or services that serve their clients and counterparts in this region, so that more of the vacant office space can be absorbed.

Rigorous efforts to market KL as a regional hub must be intensified

The office market overhang calls for a concerted effort by the government and stakeholders in the industry to promote KL as a base for foreign companies and MNCs looking to tap into the burgeoning Asian market.

The government should intensify efforts to attract investments from MNCs to set up their regional headquarters and services here as local companies might not be able to absorb the huge vacant space in KL.

“The government should set up a strong one-stop agency looking at attracting MNCs and investors in KL’s commercial real estate (such as offices) for cross-collaboration or assimilation with existing entities such as InvestKL and Mida,” says Datuk Paul Khong, managing director of Savills Malaysia.

To be fair, there have been efforts by the government to attract MNCs to set up their regional headquarters and services in KL.

Since its inception in 2011, InvestKL, an agency under the Ministry of International Trade and Industry, has been at the forefront of promoting Greater KL as an investment destination.

However, it is not the mandate of InvestKL to fill vacant office space in KL. And as a government agency, InvestKL posits itself to be independent of the private developments in the city, acting only as a guiding hand and promoter of KL to foreign investors.

“As a government agency, we must remain independent to bring in MNCs, and wherever they locate would really depend on their commercial discussions and agreements with any particular building or service provider for that matter. We do not get involved in any of those discussions,” Invest KL CEO Muhammad Azmi Zulkifli tells The Edge.

“When companies look at or evaluate locations, they look at a few other attributes — connectivity, F&B, the location, be it in the city or suburbs. All of that is put into context. We have been consistently driving investments, and so have other government agencies.

“We will be able to close the gap or address some of these vacancies, to a certain extent. We certainly cannot be and are not a party to what has been developed over the months or years with what is happening so far.”

In its first 10 years, InvestKL has managed to attract 103 MNCs to set up either their regional headquarters in the Greater KL area or services that cover organisations or clients in the region.

According to Azmi, this exceeds the target of attracting 100 MNCs into Greater KL by end-2020. And by end-2021, the number had climbed to 116 MNCs using Greater KL as their regional base.

The 103 MNCs that have set up their regional base or operations in Greater KL have brought in RM18 billion of investments, according to Azmi. This value then became the basis for the next 10-year target for InvestKL — securing RM20 billion of investments between 2021 and 2030.

However, InvestKL does not provide the statistics for office space occupied by these MNCs in the capital city. Looking at the rising number of vacant buildings in the city, it is safe to assume that there are not enough MNCs moving to KL.

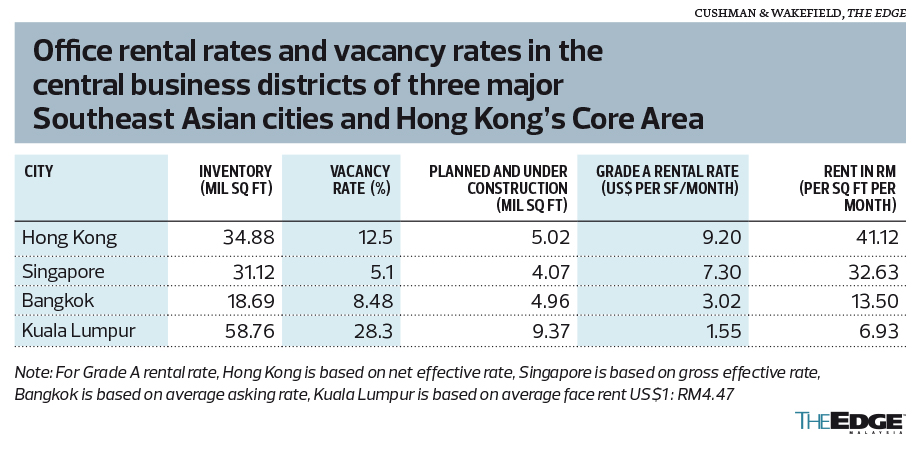

Why is this the case? After all, when comparing KL and other cities in the region such as Singapore, Bangkok and, to a certain extent, Hong Kong, it does offer investors value for money.

Looking at the rental rates of office spaces in the CBD or core areas of these cities, KL is the cheapest among them, and by a large quantum.

According to Cushman & Wakefield, the average rent per sq ft per month of office space in KL CBD is RM6.93, compared with an equivalent of RM13.50 in Bangkok, RM32.63 in Singapore and RM41.12 in Hong Kong.

“In our experience with large MNCs, they do not necessarily look at a particular category from an office space standpoint. Many other considerations are in place and office space would come right at the end of their discussion.

“However, the context of office space has a lot to do with connectivity to the location, what are the supporting services of the location, for example, F&B, as well as accommodation, and then looking at what they need as a centre in terms of the support,” says InvestKL’s Azmi.

Cities like Singapore and Hong Kong, while more expensive than KL, also provide low corporate income tax rates. This is also a consideration for MNCs that are looking to effectively reduce their tax expenses when setting up an offshore operation.

From this perspective, the Malaysian government does provide tax breaks for MNCs if they choose to make KL their regional hub and service centres. For example, under the Principal Hub Incentive 3.0, effective from Jan 1, 2021, a company could enjoy tax rates of between 0% and 5% for a total of 10 years.

A company would qualify under the Principal Hub Incentive if it uses Malaysia as a base for conducting its regional or global businesses and operations to manage, control and support its key functions, including management of risks, decision making, strategic business activities, finance, management and human resource.

However, this applies only to new companies setting up regional hubs or operations in Malaysia. Existing companies could still apply for the Principal Hub Incentive, but the lowest tax rate they can get is 10%.

This is something that Yee Wing Peng, CEO of Deloitte Malaysia, wishes the government would look into: to also allow existing companies to be eligible for the 0% to 5% tax rate under the Principal Hub Incentive.

“MNCs that are already here undertaking other activities [and] which would now like to expand into regional activities … would find that they are at a disadvantaged position compared with new MNCs,” Yee tells The Edge.

Deloitte Malaysia provides consultancy services to MNCs looking to set up their regional hubs or operations in the country. As a local arm of an MNC itself, it also provides regional services for other Deloitte offices in the region.

Its headquarters at Menara LGB in Taman Tun Dr Ismail employs around 1,800 people from 35 nationalities, Yee says, adding that Deloitte Malaysia is set for an expansion of its regional services.

However, Malaysia should not compete with Singapore or other regional cities from a taxation point of view, says InvestKL’s Azmi, as it is a race to the bottom.

The global minimum tax rate of 15% that will be implemented soon will also mean that tax havens will become a thing of the past, he adds.

In fact, he says, most of the MNCs that InvestKL has managed to attract to set up base in Greater KL did not qualify for fiscal incentives.

“Only 35% of the 116 companies are enjoying fiscal incentives in the form of tax benefits and so on. My point is, why are the other 65% choosing KL as a location? It is because of two things — the dynamic and thriving ecosystem available in Greater KL, and the ease of doing business.

“When we talk about our plans as well as our activities in the future, consistently, Malaysia has been measured in terms of our competitiveness and ease of doing business in an international survey,” says Azmi.

Investors’ perception on corruption in Malaysia must be addressed

On the flip side, Malaysia’s competitiveness as a regional hub is seen to have been negatively affected by the high perception of corruption.

According to Savills Malaysia’s Khong, while KL has always been considered one of the cheapest real estate platforms in the region, where both rents and capital value are relatively low, the city still lags behind Singapore in terms of its ranking on the Corruption Perceptions Index (CPI).

“The perceived level of corruption is a major challenge in attracting global businesses here and is further exacerbated by landmark scandals of late,” says Khong in an email response to The Edge.

In 2021, Malaysia’s CPI score of 48 lagged behind Singapore’s score of 85, which is the second highest in the world, after Denmark, Finland and New Zealand, which all had 88 points. This shows the low level of corruption in Singapore.

Malaysia’s CPI score of 48 puts it on a par with Armenia, Greece, Jordan, Namibia, Croatia, Cuba, Montenegro, China, Romania, São Tomé and Príncipe and Vanuatu — countries that, except for China, are not usually known as investment hotspots for MNCs.

In Southeast Asia, however, Malaysia’s score is the second highest, ahead of Vietnam (39), Indonesia (38), Thailand (35) and the Philippines (33).

InvestKL’s Azmi says the MNCs that have approached the agency for advice or assistance to set up their regional hubs or operations in Greater KL must have done their own research on the perceived risks of investing in Malaysia.

In fact, InvestKL is firm about its stance against any forms of side deals being asked whenever an MNC is looking to set up its regional operations in the city.

Azmi says: “If they bring it [the CPI] up, we certainly will not defend it, because that is a third party and independent study. But we will also try to put into perspective what our role is. Our role is to attract investments and facilitate investments, making sure we bring you in, and we handhold you throughout the process.

“That means we will be there along the way to ensure the ease of doing business, which also means that we will not allow any form of side deals being asked from that perspective.”

To attract MNCs to set up their regional hubs and services here, the strengths of Malaysia and KL need to be promoted and policies need to be implemented to make it much easier for MNCs to set up their operations.

Already, Malaysia has been doing well in the World Bank’s Ease of Doing Business Index (or Business Enabling Environment Index since 2021). In 2020, the country ranked 12th in the world, coming in first among developing countries in Asia. However, Malaysia still lags behind Singapore, which ranked second globally in ease of doing business. Since the country is competing against Singapore in attracting MNCs to set up their regional hubs, Malaysia’s shortfalls will be Singapore’s gains.

Nevertheless, InvestKL’s Azmi is optimistic about the KL’s prospects of attracting MNCs because many MNCs are looking at a dual-hub strategy when it comes to choosing their regional hubs.

“When we talk about the dual-hub concept — that is, managing risk, where one may not want to put all of one’s important people in the same location — they may want to split the locations to address some of these risks.

“And that is why we have seen companies have also exploited this dual-hub concept — having some form of activities in Singapore and a larger installation in Greater KL,” says Azmi.

According to him, InvestKL has successfully relocated a number of MNCs from the two traditional locations for regional headquarters — Singapore and Hong Kong — to the Greater KL region. He says that when a company looks at its regional hub set-up, it tends to look at a three-, five- and ten-year horizon.

“When they ran the numbers, it didn’t look sustainable for them to have 500 people in a very expensive location, and that is where Greater KL is playing into that particular niche, to provide that balance of locations,” says Azmi, adding that Greater KL is just second to its competitors when it comes to infrastructure, connectivity and so on.

KL has many things going for it. So, let’s roll out the red carpet to welcome more MNCs to set up their regional hubs in the capital city and populate the empty office buildings.